A FIRE calculator tells you two things that matter more than almost any other number in personal finance: how much you need to retire early, and exactly when you will get there. Plug in your annual expenses, current savings, monthly contributions, and expected investment returns — and the calculator returns your FIRE number and the year you can stop trading time for money.

The right calculator does not just spit out a target. It helps you stress-test assumptions, see how small changes compound over decades, and — if you are location-independent — compare FI dates across different countries. This guide walks you through what a FIRE calculator actually does, the six inputs that move the needle, and a step-by-step walkthrough using IndepAI’s FI Calculator.

What is FIRE?

FIRE stands for Financial Independence, Retire Early. The idea is simple: save and invest aggressively enough that your portfolio generates sufficient returns to cover your living expenses indefinitely. Once your investments can sustain your lifestyle without you needing to work, you are financially independent.

The movement has several flavors:

- Lean FIRE — minimalist lifestyle, $25,000 to $40,000 annual spending

- Regular FIRE — middle-class lifestyle, $40,000 to $60,000 annual spending

- Fat FIRE — premium lifestyle, $100,000 or more annual spending

- Coast FIRE — your current savings will grow to your target without further contributions

- Barista FIRE — partial portfolio plus part-time income covers expenses

Each variant has its own math, but they all share a common engine: the FIRE calculator.

How a FIRE Calculator Works

At its core, a FIRE calculator executes three steps:

1. Compute your target portfolio. Most calculators use the 4% rule: multiply your annual expenses by 25. If you spend $60,000 per year, your FIRE number is $1,500,000. The 4% rule comes from the 1998 Trinity Study, which showed that a 50/50 stock-bond portfolio withdrawing 4% annually (adjusted for inflation) survived nearly all historical 30-year retirement windows.

2. Project your portfolio’s growth. Using your current savings, expected monthly contributions, and an assumed real rate of return (typically 5 to 7 percent after inflation), the calculator projects your portfolio value year by year. This is compound interest doing the heavy lifting.

3. Find the crossover year. The year your projected portfolio equals or exceeds your target is your FI date. That is the year you could, in theory, stop working and live off your investments indefinitely.

A good calculator also shows you the sensitivity: how the date shifts if you save $500 more per month, if returns come in at 5% instead of 7%, or if you cut annual expenses by $10,000.

Calculate Your FIRE Number

Use the interactive calculator below to find your exact FIRE number and FI date. Adjust inputs to see how each lever affects your timeline.

FI Calculator

Calculate your path to Financial Independence. Enter your financial details below.

Savings rate: 40.0%

Want to try this on your own numbers at launch? IndepAI is in private build right now, so join the waitlist for priority access and help shape what we build first. →

The 6 Inputs That Actually Matter

Many calculators ask for a dozen parameters. In reality, six move almost everything:

1. Annual Expenses

This is the single most powerful input. Your FIRE number is a multiple of what you spend, not what you earn. A household spending $40,000 per year needs $1,000,000. A household spending $80,000 needs $2,000,000. Every $1,000 of annual spending adds $25,000 to your FIRE target.

This is why frugality compounds so brutally in the FIRE community: cutting $500 per month in recurring costs reduces your target by $150,000 and typically pulls in your FI date by two to four years.

2. Current Portfolio Value

The starting balance in your investment accounts (401k, IRA, taxable brokerage, index funds, real estate equity if you count it) determines how much compound growth has already been set in motion. A $200,000 starting portfolio growing at 7% adds $14,000 in its first year — passive income that did not exist when you had nothing invested.

3. Monthly Contribution

How much new money you invest each month. Your savings rate — contributions divided by take-home pay — is the best single predictor of your FI timeline. A 50% savings rate reaches FI in roughly 17 years. A 25% savings rate takes closer to 32 years. A 70% savings rate reaches FI in under 10.

4. Expected Real Rate of Return

This is the assumed annual growth of your portfolio after inflation. Common choices:

- 7% — long-run global equity real return, historically defensible

- 5 to 6% — conservative, recommended for planning margins of safety

- 4% — very conservative, often used by retirees already in withdrawal

Never use nominal returns (unadjusted for inflation). A 10% nominal return with 3% inflation is a 7% real return, and if your expenses are in today’s dollars, you must use real returns or you will underestimate your target.

5. Target Withdrawal Rate

The 4% rule is the default, but 3.25 to 3.5 percent is increasingly common for early retirees with 40-plus-year horizons. Lower withdrawal rates mean a larger FIRE number but far more resilience against sequence-of-returns risk.

6. Your Target Country / Cost of Living

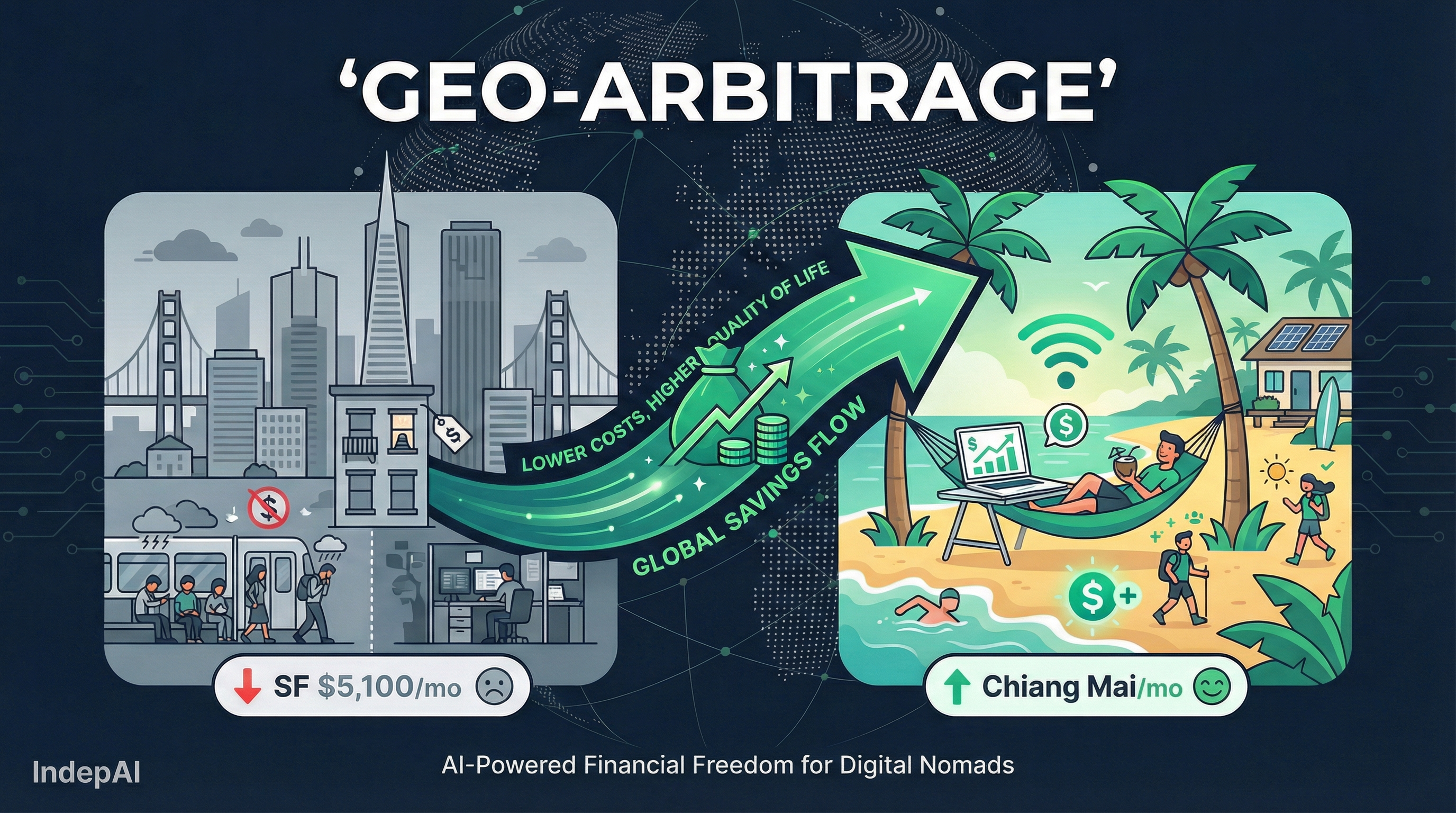

Almost no general-purpose FIRE calculator asks this. But if you are willing to retire abroad, your cost of living can drop 40 to 60 percent. Geo-arbitrage is the single most powerful shortcut in the FIRE playbook, and a calculator that ignores it will overstate your target by hundreds of thousands of dollars.

Step-by-Step Walkthrough with IndepAI

Let us run a real scenario through the IndepAI FI Calculator.

Meet Sarah. She is a 34-year-old remote software engineer living in San Francisco.

- Annual expenses: $80,000

- Current portfolio: $180,000

- Monthly contributions: $3,500

- Expected real return: 7%

- Target withdrawal rate: 4%

Step 1: The baseline calculation.

Sarah’s FIRE number is $80,000 times 25 = $2,000,000.

At $3,500 per month contributions and 7% real returns, her current $180,000 portfolio reaches $2,000,000 in approximately 17 years. She would hit FI at age 51.

Step 2: Stress-test with a lower return.

Sarah drops her assumption to 5% real return. Her FI date slips to approximately 21 years — age 55. That four-year delta is the price of optimism.

Step 3: Apply geo-arbitrage.

Sarah considers retiring in Lisbon. Her $80,000/year San Francisco lifestyle costs roughly $48,000 in Lisbon (rent drops from $2,800 to $1,100, groceries, dining, and healthcare all fall). That is a 40% cut in spending.

Her new FIRE number is $48,000 times 25 = $1,200,000 — $800,000 lower.

At the same $3,500/month contribution and 7% real return, she reaches $1,200,000 in approximately 11 years instead of 17. She retires at age 45 in Lisbon instead of age 51 in San Francisco.

That is six years of her life returned to her, purely by changing her target location. This is the kind of analysis a generic calculator cannot perform. IndepAI’s FI Calculator lets you swap target cities inline, compare FI dates side by side, and factor in visa and tax regimes. See the best countries for FIRE in 2026 for a breakdown of the top 20 destinations.

Step 4: Increase the savings rate.

If Sarah pushes her monthly contribution to $4,500 while still planning for Lisbon, she hits $1,200,000 in roughly 9 years — at age 43. Each extra $1,000 per month shaved approximately two years off her timeline.

Common Mistakes

1. Using Nominal Instead of Real Returns

If your annual expenses are in today’s dollars and you project your portfolio with nominal returns, you will systematically underestimate your target. Always use real (inflation-adjusted) returns, or inflate both sides of the equation.

2. Ignoring Healthcare

In the US, pre-Medicare healthcare can cost $600 to $1,200 per month per person on marketplace plans. A couple retiring at 45 may need $240,000 in extra cushion just for 20 years of health insurance premiums before Medicare kicks in. Many FIRE calculators do not separate this line item.

3. Assuming Static Expenses

Kids grow up. Mortgages get paid off. Elder care emerges. Your spending at 40 is not your spending at 65. Advanced FIRE calculators let you model stepped spending (higher during child-rearing years, lower afterward); simpler ones do not. If yours does not, run the scenario twice with both numbers.

4. Forgetting Taxes

Traditional 401k and IRA withdrawals are taxed as income. A $2M portfolio is not $2M of spendable wealth — it might be $1.5M to $1.7M after taxes depending on your withdrawal strategy and residence. Tax-efficient withdrawal sequencing and residence in a low-tax jurisdiction can materially change your timeline.

5. Treating the FIRE Number as a Finish Line

FIRE is not a single point. It is a probability distribution. Hitting your number with a 95% success rate is different from hitting it with a 70% success rate. Monte Carlo-style calculators show you the distribution of outcomes; simple deterministic ones give you a single line. Use both.

6. Optimizing Only One Side of the Equation

Most FIRE calculator users obsess over the savings rate and ignore the expenses side. But expenses are the multiplier. Cutting $10,000/year in expenses removes $250,000 from your target and often saves more time than a $500/month raise in contributions. Audit your expenses before you optimize your contributions.

Frequently Asked Questions

What is a FIRE calculator?

A FIRE calculator is a financial planning tool that estimates the amount of invested assets you need to cover your living expenses indefinitely, plus the number of years until you reach that number based on your current savings rate, portfolio value, and expected investment returns. Most FIRE calculators apply the 4% rule, multiplying your annual expenses by 25 to produce a target portfolio, then projecting compound growth against your monthly contributions.

How do I calculate my FIRE number?

Multiply your annual expenses by 25 to get your FIRE number using the 4% rule. For example, $80,000 in annual spending produces a $2,000,000 target. For a more conservative plan, multiply by 28 (a 3.5% withdrawal rate) or by 33 (a 3% rate). A good FIRE calculator does this automatically and then projects how many years of saving and investing are required to reach that portfolio at your current contribution rate.

Is the 4% rule still accurate in 2026?

The 4% rule, based on the 1998 Trinity Study, remains a reasonable starting point but is not bulletproof. For retirement horizons longer than 30 years (common in early retirement), many planners now recommend 3.25 to 3.5 percent. Sequence-of-returns risk, elevated equity valuations, and longer life expectancy all argue for a slightly more conservative withdrawal rate or a flexible spending plan that responds to market conditions.

Can a FIRE calculator account for geo-arbitrage?

Most generic FIRE calculators cannot. They assume you stay in one country with one cost of living. IndepAI is built specifically for location-independent FIRE planning: you can compare your FI date in Lisbon versus New York versus Chiang Mai, factor in visa and tax regimes, and see how a move cuts your target portfolio by 30 to 50 percent. A $2M target in San Francisco often becomes a $1.2M target in Lisbon for the same lifestyle.

How often should I recalculate my FIRE number?

Revisit your FIRE number at least annually and after any major life event: a raise, a move, a relationship change, a new child, a health diagnosis, or a shift in your target retirement country. Small changes in annual expenses compound enormously: cutting $5,000 per year in spending reduces your FIRE number by $125,000 at a 4% withdrawal rate, potentially shaving three to five years off your timeline.

Be First to Try IndepAI

IndepAI isn’t live yet. We’re building the first FIRE planner with geo-arbitrage, visa, and tax-regime support baked in. Waitlist members get priority early access and a say in what we ship first.

- Join the IndepAI waitlist — Be first to try a city-aware FIRE planner across 11,400+ destinations

- Coast FIRE Guide — Learn the Coast FIRE variant and when you can stop saving entirely

- Best Countries for FIRE in 2026 — The top 20 destinations ranked by cost of living, tax regime, and visa accessibility

Know your number. Know your city. Know your date.

They told you to save harder. Check the city lever.

Most FIRE calculators assume you never move. IndepAI shows how your FI date changes when your city changes.

Private build. No spam.