Coast FIRE is the point where your current savings, left alone to compound, will reach your full Financial Independence number by retirement age. Hit it and you can stop saving entirely. From then on you only need to earn enough to cover today’s expenses.

Regular FIRE (Financial Independence, Retire Early) asks you to save hard until your investments can cover everything, indefinitely. Coast FIRE hands you an earlier milestone, the moment the pressure to save lifts. Cross that line and time does the rest of the work for you.

How Coast FIRE Works

The idea is simple. Figure out what your current investments will be worth at retirement, then check whether that number clears your target. The formula is one line.

Coast FIRE Number = FI Target / (1 + r)^n

Here FI Target is the portfolio you want at retirement, often 25x your annual expenses under the 4% rule. The letter r is your expected annual real return after inflation, usually somewhere between 5 and 7%. And n is the number of years until you retire.

Say you are 30, have $100,000 invested, expect a 7% return, and want $1,000,000 by age 60. Your Coast FIRE number works out to $1,000,000 / (1.07)^30, which is $1,000,000 / 7.612, or $131,367.

You are close, but not quite there. With $100,000 saved you need about $31,000 more. Once you cross $131,367, though, you could stop contributing to retirement accounts completely and that balance would still grow to $1,000,000 by age 60 at 7% a year. If you expect to spend $40,000 a year in retirement, the 4% rule puts your target at $1,000,000, which is exactly why $131,367 today is your Coast FIRE number.

Calculate Your Coast FIRE Number

Use the interactive calculator below to find your personal Coast FIRE number. Adjust your current age, savings, expected returns, and retirement target to see exactly where you stand.

Coast FIRE Calculator

Calculate how much you need saved today to coast to Financial Independence without additional contributions

Savings rate: 40.0%

Coast FIRE vs Other FIRE Types

Coast FIRE is one of several flavors, each built for a different lifestyle and risk appetite:

| FIRE Type | Annual Spending | Portfolio Needed (4% Rule) | Key Idea |

|---|---|---|---|

| Lean FIRE | $25,000-$40,000 | $625K-$1M | Minimalist lifestyle, lower target |

| Coast FIRE | Varies | Current savings grow to target | Stop saving, just cover expenses |

| Barista FIRE | $40,000-$60,000 | Partial portfolio + part-time income | Semi-retirement with some work |

| Regular FIRE | $40,000-$60,000 | $1M-$1.5M | Full financial independence |

| Fat FIRE | $100,000+ | $2.5M+ | Maintain a premium lifestyle |

Lean FIRE is for minimalists who can live well on $25,000 to $40,000 a year; calculate your Lean FIRE number to see how a frugal lifestyle pulls your timeline forward. Barista FIRE assumes part-time work covers the gap between your portfolio and your spending, and the Barista FIRE calculator finds that number for you. Fat FIRE goes the other way, funding a $100K+ lifestyle in retirement, and the Fat FIRE calculator shows what that takes.

What sets Coast FIRE apart is that it is not tied to a spending level at all. It is a savings threshold, and once you pass it, compound growth covers the rest. That is also why it is the most freeing milestone of the bunch. The constant pressure to save simply goes away.

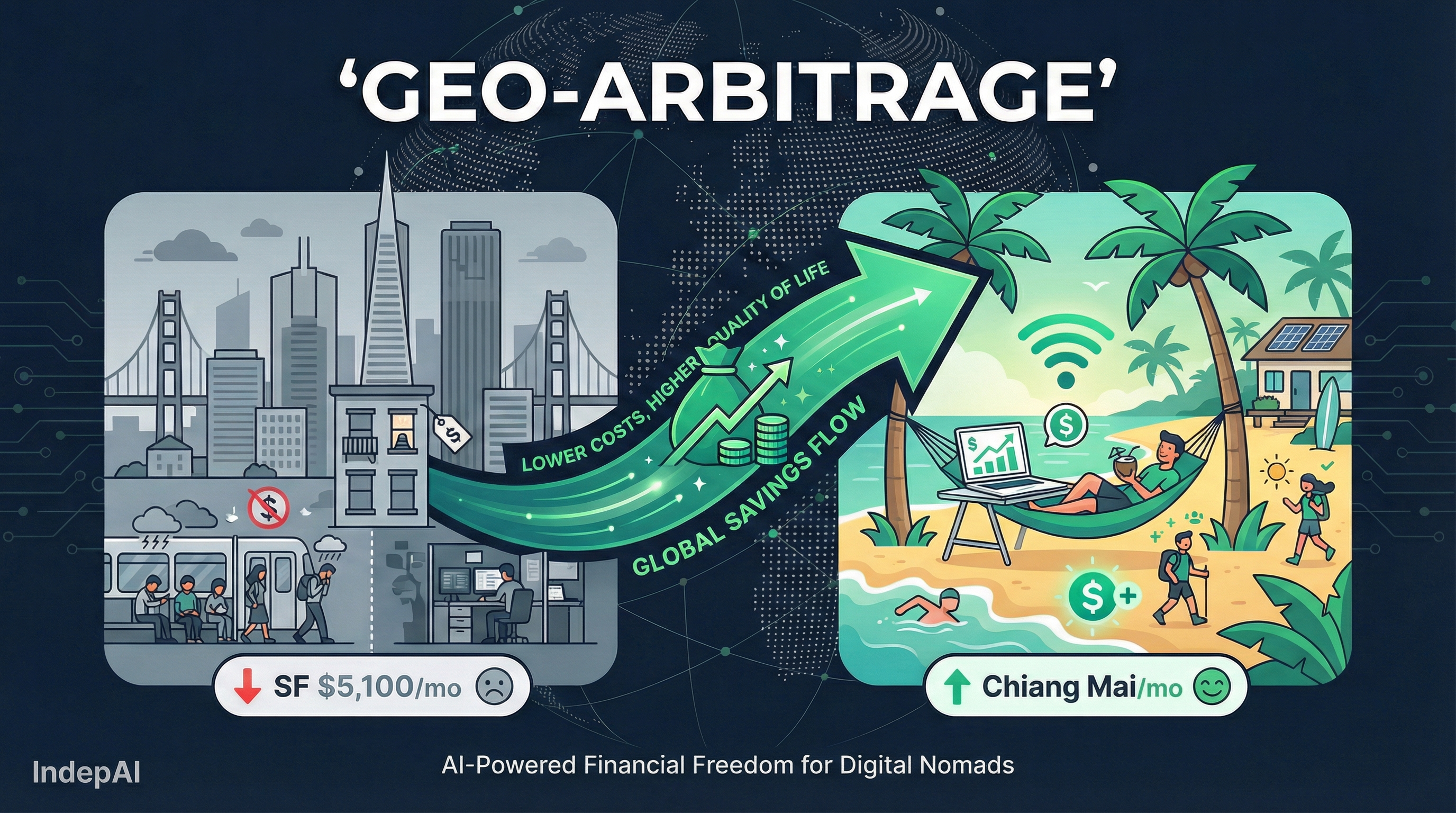

Coast FIRE for Digital Nomads

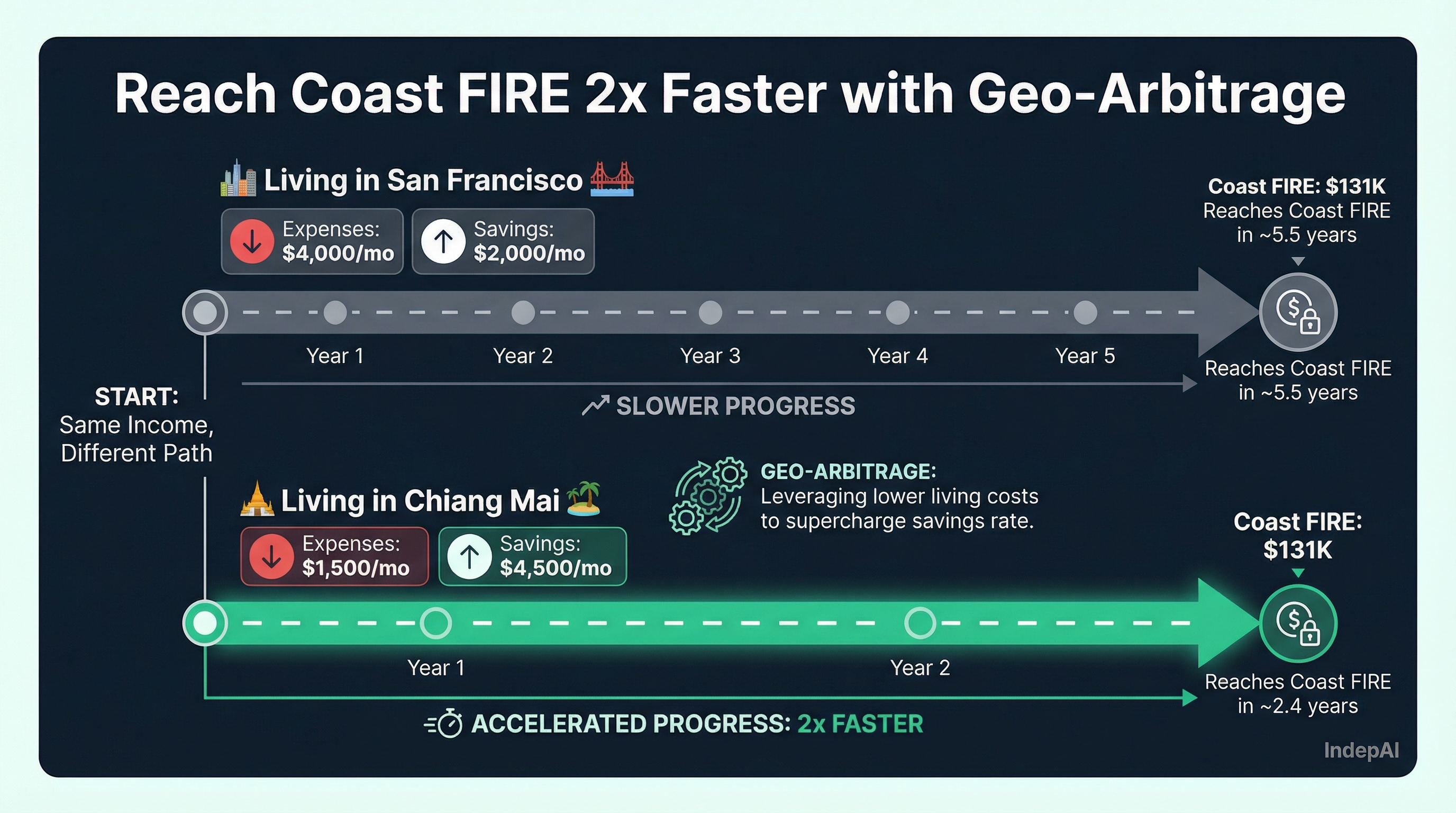

If you work remotely, geo-arbitrage can cut your path to Coast FIRE roughly in half.

Geo-arbitrage means earning in a strong currency like USD, EUR, or GBP while living somewhere cheaper. Done during your accumulation years, it can double or triple your savings rate and bring your Coast FIRE number forward by years.

Picture the same $6,000 income in two places. In San Francisco you spend $4,000 a month and save $2,000. In Chiang Mai you spend $1,500 and save $4,500 on the identical paycheck. At that savings rate you hit your Coast FIRE number in about half the time, and because your cost of living stays low, you need even less income once you start coasting.

Use the geo-arbitrage tool to compare cities and see how location changes your FI timeline. It pairs FIRE planning with real cost-of-living data, so you can watch a move to a different city reshape your path to financial freedom.

Common Coast FIRE Mistakes

1. Ignoring Inflation

A 7% nominal return is not a 7% real return. If inflation averages 3%, your real return is closer to 4%. Always use real (inflation-adjusted) returns in your Coast FIRE calculation, or adjust your target upward for future inflation. Underestimating inflation is the most common reason people fall short of their Coast FIRE targets.

2. Assuming Constant Returns

Markets do not return a steady 7% per year. Some years you gain 25%, others you lose 20%. Sequence-of-returns risk is real: a major downturn early in your coasting period can permanently reduce your portfolio’s growth trajectory. Build in a 10-20% margin of safety above your calculated Coast FIRE number.

3. Not Accounting for Healthcare

If you plan to coast in your 30s or 40s, you may face decades without employer-sponsored health insurance. In the US, marketplace plans can cost $400-$800/month for an individual. Factor it into your coasting expenses. It is a significant line item that many Coast FIRE calculators quietly ignore.

4. Forgetting About Lifestyle Inflation

Your expenses at 30 may look very different from your expenses at 50. Marriage, children, aging parents, and changing health needs can all increase spending. Periodically re-evaluate your Coast FIRE number as your life circumstances evolve.

5. Neglecting Tax-Advantaged Accounts

Even after reaching Coast FIRE, it may still make sense to contribute to tax-advantaged accounts (401k match, Roth IRA) while you are earning income. The tax benefits compound over time and add a layer of security. Coast FIRE does not mean abandoning every financial optimization. It just means you no longer need to save at a high rate.

Frequently Asked Questions

How much money do I need for Coast FIRE?

Your Coast FIRE number depends on your age, target retirement age, expected investment returns, and desired retirement spending. For example, a 30-year-old targeting $1M at age 60 with 7% returns needs roughly $131,000 saved today. Use our Coast FIRE calculator above to find your exact number.

What is the difference between Coast FIRE and regular FIRE?

Regular FIRE requires you to save and invest aggressively until your portfolio covers all living expenses indefinitely. Coast FIRE is the point where your existing savings will grow to your full FIRE number through compound interest alone, meaning you only need to earn enough to cover current expenses without saving anything additional.

Can I achieve Coast FIRE faster with geo-arbitrage?

Yes. Geo-arbitrage dramatically accelerates Coast FIRE by reducing your current living expenses. If you earn in USD or EUR while living in a lower-cost country, you can save more aggressively in the early years, reaching your Coast FIRE number sooner. Once you hit Coast FIRE, your reduced expenses also mean you need less income during the coasting phase.

What rate of return should I assume for Coast FIRE calculations?

Most financial planners use 7% nominal return (roughly 10% market return minus 3% inflation) for long-term stock market investments. Conservative planners may use 5-6%. The key is to stay consistent and realistic. Overly optimistic assumptions can breed a false sense of security.

Is Coast FIRE safe? What are the risks?

Coast FIRE carries risks including sequence-of-returns risk (poor market performance early on), inflation exceeding expectations, and unexpected expenses like healthcare. It is important to build in a margin of safety, maintain an emergency fund, and periodically re-evaluate your Coast FIRE number as circumstances change.

Related Tools

Ready to plan your path to Coast FIRE? These tools can help:

- Coast FIRE Calculator. Calculate your exact Coast FIRE number with personalized inputs.

- FI Calculator. See your full Financial Independence timeline and milestone tracking.

- Geo-Arbitrage Tool. Compare cities worldwide and see how location affects your FI date.

Know your number. Know your city. Know your date.

They told you to save harder. Check the city lever.

Most FIRE calculators assume you never move. IndepAI shows how your FI date changes when your city changes.

Private build. No spam.